2022. 6. 30. 11:25ㆍ카테고리 없음

삐뚫어진 안경으로만 바라보던 집값시장,

할말도, 할 자격도 없지만, 채권투자물 가치의 하락 곡선이 인상적이라서 한번 옮겨본다. 전 세계적으로, ironcally enough, 코로나 사태 이후 더욱 자산시장, 특히 부동산 시장으로 돈이 몰리면서 리스크는 커졌고

아마도 몇십년만에 처음으로 두자릿수 하락률 12%를 기록했다고 한다

이하는 오늘자 블룸버그 코멘트

If there was one data item that speaks to the issues of the moment, it was the publication of the S&P Case-Shiller house price indexes. These appear with a big lag, but help to confirm that house prices have come a long way. The latest year-on-year increase is the greatest since the inception of the 20-city index in 2000. For plenty of reasons that are now well canvassed, that’s disquieting:

An overheated housing market is one of the more important reasons why the Federal Reserve is raising rates. The key question now is whether the sector can be brought into some kind of even keel without causing an accident along the way. And which parts of the financial system might be the most vulnerable.

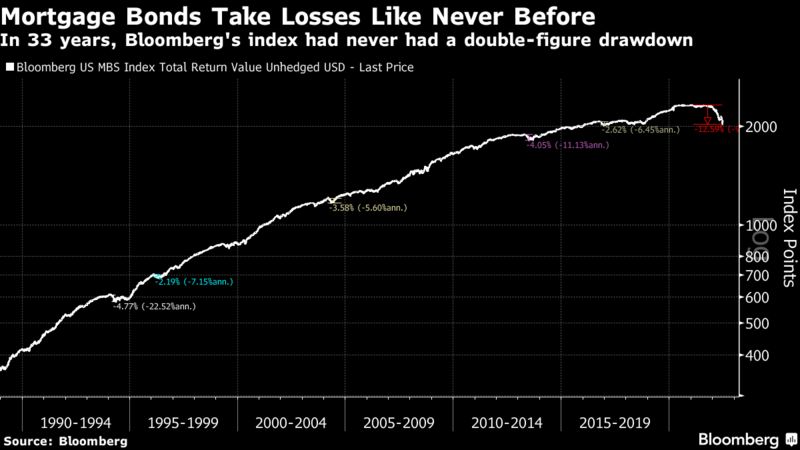

The Fed’s rate hikes have already had a dramatic effect on the mortgage market. Bloomberg’s index of US mortgage-backed bonds, including only those backed by agencies such as Fannie Mae with an implicit government guarantee, have given back all their gains of the last five years:

The percentage loss, before the recent bounce, was only about 12%. They’ve held up far better than stocks. But this is a market in which investors really don’t expect to have to put up with drawdowns. In historical context, what’s happened to mortgage-backed bonds this year is a radical departure. Bloomberg’s index dates back to 1988, when the asset class was still in its infancy. This is the first time it has ever withstood a decline that stretches into double figures:

This looms as a serious shock to anyone who was relying on mortgage-backed bonds to hold their value. That doesn’t apply to banks particularly, which in the US were forced to sort out their act in the wake of the disasters of 2008. But as has often happened in the past, tighter regulation in one sector drove financial innovation into new places. Just as money market mutual funds developed to allow investors to avoid paying for deposit insurance, as they would have to do on funds held in banks, so non-bank financial institutions have been able to seize yet more business that would once have been done by traditional lenders. This chart by London’s Absolute Strategy Research Ltd. demonstrates the strength of global non-bank financials compared to their orthodox peers. After a collapse in 2008, a new range of non-banks has emerged whose market cap has grown much faster than the incumbents:

The new nimbler players have quickly established a big share of the mortgage market. This chart, drawn by Absolute Strategy from bankrate.com data, shows the 10 biggest originators in the US last year. Most non-Americans will only have heard of two; and very few Americans will have heard of all of them:

Logic and experience therefore guide us to look into the mortgage market for points of vulnerability. As Absolute Strategy puts it, these companies have “untested business models, and are large enough to create potentially systemic risks for policy makers.” The biggest originator, Rocket Cos Inc., based in Detroit, is a good exemplar. My Bloomberg Intelligence colleague David Havens produced the following chart, which sums up the dynamics in play neatly enough. As Treasury rates rise, so the spreads on Rocket’s bonds widen, while its share price falls: